Medicare Advantage, the form of Medicare where insurance companies take the risk of monetary losses while providing the same care as traditional Medicare but at a lower cost to beneficiaries, now provides the majority of care to Medicare-eligible individuals. That risk was well worth it. Moody’s, while noting that year-to-year revenue has increased and declined over time, points out that the earnings per beneficiary are double that earned through insuring Medicaid patients and 45% more than what is earned on beneficiaries with commercial insurance (those under age 65, not enrolled in Medicare).

Only the mathemagicians of insurance administration can charge beneficiaries less, give them “more,” and still show a significant profit. There are many accounts (here, here, and here) of how those mathemagicians upcode charts to create beneficiaries who are virtually more ill than in reality and reap additional risk adjustments from Medicare. And denial of care has had a great deal of play in the news, given the tragic events in New York City with United Healthcare’s CEO Brian Thompson

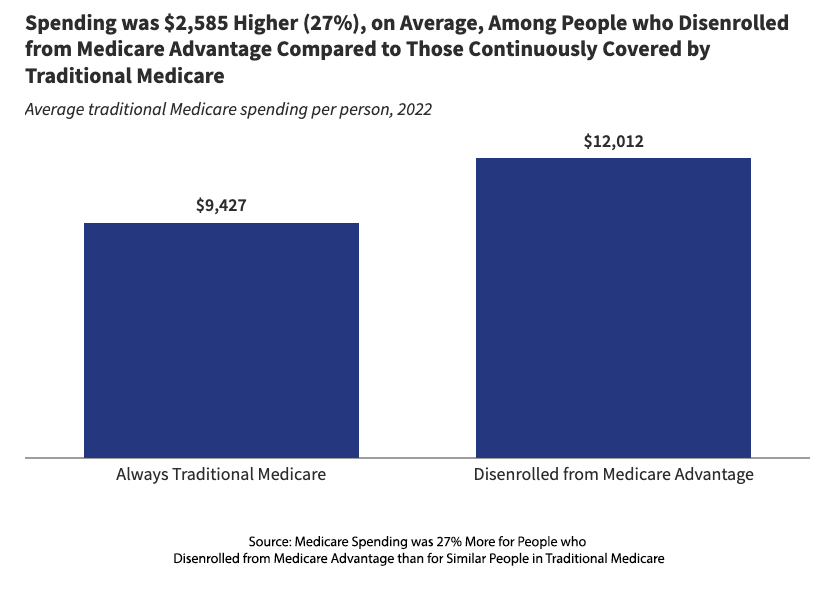

A few days ago, the annual Medicare enrollment period for starting, ending, or switching an individual's Medicare Advantage (MA) plan ended. A new study by the Kaiser Family Foundation examines how much more is spent by an individual disenrolling from MA and re-enrolling in Traditional Medicare.

After disenrolling, Medicare paid $2,585 more in the next year – an increase of 27% in the cost of care if the beneficiary had been enrolled in traditional Medicare the entire time. In other words, MA advantages insurance companies when enrolling and disenrolling a beneficiary – they get us coming and going.

The report details variations in the increase in spending by diagnosis, e.g., 34% higher for individuals with diabetes, 15% for those with pneumonia; with increasing age, e.g., 47% higher for those age 85+ compared to 25% for those 65-69; 61% more for those “dual eligible,” having both Medicare and Medicaid vs. 20% not requiring Medicaid.

A deeper dive revealed that the more significant costs to Medicare in that next year were for hospital services, outpatient, inpatient, and post-acute care (meaning nursing home or home health care). Post-acute care reflected the majority of those costs shifted from MA to Medicare.

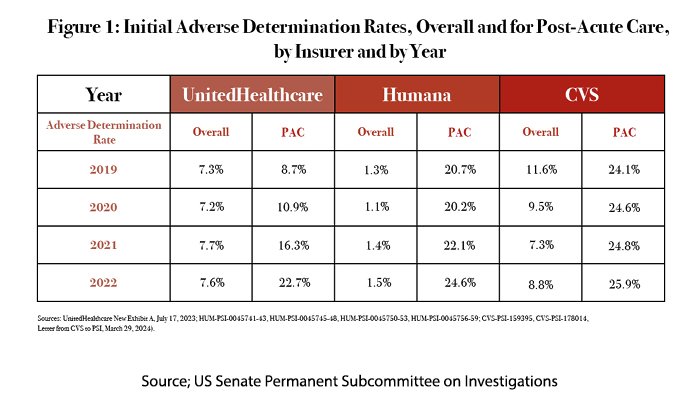

The findings align with a study conducted by the US Senate’s Permanent Subcommittee on Investigations, which looked at post-acute care denials by United Healthcare, CVS, and Humana, the three largest MA providers covering 60% of the market. While both Medicare and MA must provide care that is “reasonable and necessary for the diagnosis or treatment of an illness or injury,” Medicare determines necessity after the care has been rendered. MA programs make that determination before care, prior authorization (PA).

These prior authorizations are handled, as much as possible, digitally. As the Senate report indicates, in 2022, MA received 46 million PA requests, denying about 7.4% or 3.4 million (This does not include the separate appeals). The human workforce necessary to process those requests would easily bankrupt these organizations, so much of the approval process has been turned over to algorithms. Much of the consternation of late over PA has been the application of “artificial intelligence” to those algorithms that more quickly and efficiently deny care. [1]

For those over 65 undergoing care requiring hospitalization, either outpatient or inpatient, there is often a need, because of those pesky co-morbidities, for some degree of rehabilitation to return to their former spry self – to fully resume the activities of daily living. Whether delivered in your home or a skilled nursing facility (SNF), these services are labor-intensive and costly. MA programs have a long history of providing these services at lower rates to their beneficiaries than traditional Medicare. In the last few years, the mathemagicians have turned up the volume on those denials.

Overall refers to all denials, PAC to post-acute care denials. Their work has been dramatically accelerated by these machine-learning algorithms. NaviHealth, a subsidiary of United Healthcare, has sold this algorithm to other insurers.

The voices on the Internet have suggested that in the face of rising costs, MA programs will have to:

- Reduce spending

- Increase beneficiary premiums

- Leave the market

There is a fourth option, the one pursued by, among others, United Healthcare. Last year, they purchased LHC, a home healthcare company, gobbling up a “cost center” and creating a new revenue stream.

“LHC Group, Inc. is a national provider of in-home healthcare services and innovations for communities around the nation, offering quality, value-based healthcare to patients primarily within the comfort and privacy of their home or place of residence. … – reaching 68 percent of the US population aged 65 and older. LHC Group is the preferred in-home healthcare partner for more than 400 leading hospitals around the country.”

United Healthcare’s attempt to purchase Amedisys is currently under an anti-trust suit by the Department of Justice. Kindred Healthcare, the largest home care provider, is owned by Humana. All of these purchases are attempts at vertical integration – when a company expands control over multiple stages of the supply chain or production. In the case of United Healthcare, it has extended control by purchasing medical practices (at scale), pharmacy benefit management, and now downward integration into home health care.

While vertical integration is not inherently anti-competitive when it forecloses competition, enables price discrimination, or erects barriers to the entry of other companies, anti-trust concerns arise. The acquisition of home healthcare companies would reduce post-acute care denial almost immediately as United Healthcare directs its MA beneficiaries to their captured firms – in the end, simply transferring money from one pocket to another.

Medicare Advantage might look like a win-win for insurers and beneficiaries, but it remains Three-Card Monte. Scratch beneath the surface, and you'll find a carefully engineered system of cost-shifting, care denials, and monopoly-building, controlling every step of the supply chain, from doctor’s offices to home healthcare. The continued privatization of Medicare, which is what Medicare Advantage has become, will bring wealth to the shareholders, but it remains unclear whether it will truly bring hassle-free health to its beneficiaries.

[1] I have written from my personal experience that denying care is a quick means of eliminating a majority of requests. As the Senate investigation reports, only 10% of those denials are appealed, although the majority of those reverse the denial.

Chuck Dinerstein, MD, MBA

Director of Medicine

Dr. Charles Dinerstein, M.D., MBA, FACS is Director of Medicine at the American Council on Science and Health. He has over 25 years of experience as a vascular surgeon.